Ramsdens Holdings: how sustainable is the uplift?

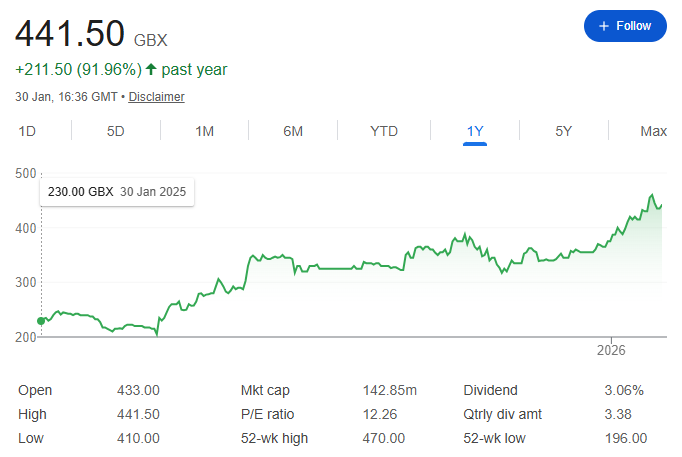

Shares in Ramsdens Holdings have risen sharply over the past year, alongside a clear improvement in both turnover and profitability. The business appears to be in much better shape than it was, but the key question for investors is whether the shares now offer a good entry point or whether that improvement is already reflected in the valuation.

The company’s mid-January full-year results presentation confirmed strong trading into the new financial year. This analysis draws on that presentation and the subsequent Investor Meet Q&A to assess whether the business is being fairly valued, and to what extent current profitability is dependent on the sharp rise in the gold price.

Business model

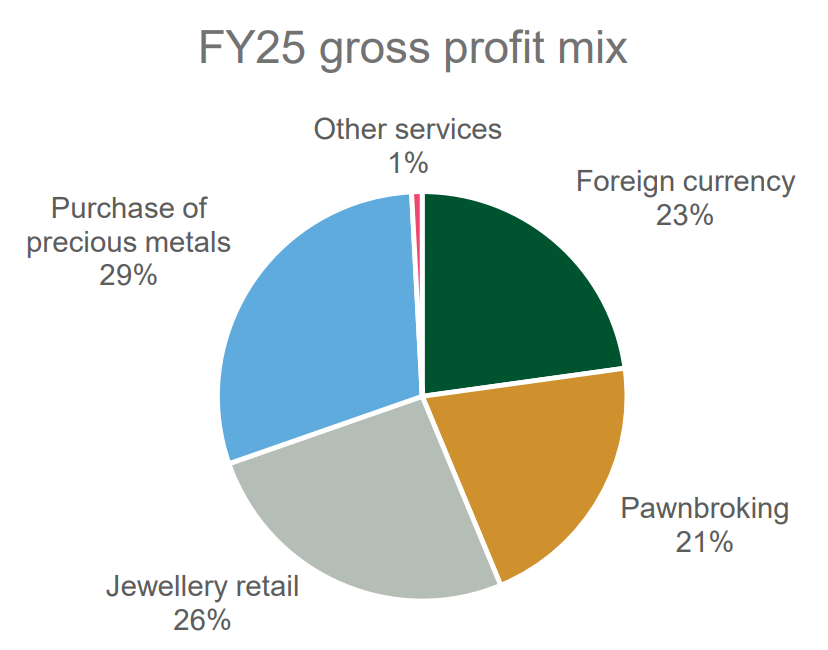

Ramsdens Holdings generates gross profit from four operating activities that are now broadly similar in scale, reducing reliance on any single revenue stream and helping explain why recent profit growth has been more resilient than a simple “gold price proxy” view would suggest.

Each activity has different drivers, capital requirements and sensitivities, but all are anchored in physical assets or transactional income rather than unsecured credit.

Purchase of precious metals

The purchase of precious metals, predominantly gold, is the most visible contributor to recent growth. Customers sell unwanted jewellery directly to Ramsdens, which then either sells the metal into the bullion market or channels it into its own jewellery retail operation.

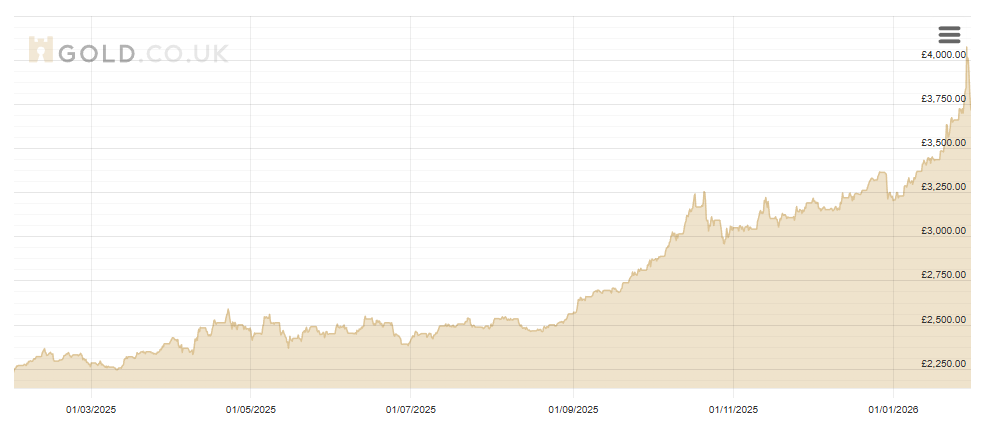

Higher gold prices have lifted both volumes and margins, with transaction sizes increasing and new sellers entering the market. This creates operating leverage beyond the headline price move.

That said, management is clear that this activity is cyclical rather than structural. Gold buying is treated as an earnings lever when conditions are favourable, not a foundation that the business depends on to remain profitable. The lack of structural debt gives Ramsdens flexibility over when and how gold inventory is sold.

Foreign currency

Foreign exchange is a steadier, lower-profile contributor. Ramsdens focuses on retail FX rather than wholesale volumes, with the average transaction margin c.3% on selling and c.10% on buying. On average, sale transactions are £400 and buy transactions are £160, and customers are generally exchanging and returning less money than they used to.

This business is capital-light and benefits from in-store footfall generated by other services. Volumes fluctuate with travel patterns, but margins are predictable and costs are largely fixed. As a result, FX provides a stabilising influence on group gross profit.

Pawnbroking

Pawnbroking remains central to earnings quality and risk control. Loans are short term, typically six months, with interest accruing daily. They are secured against gold, silver, diamond jewellery or prestigious watches.

A notable development is that Ramsdens now lends a higher proportion of an item’s intrinsic value than in the past. Loan-to-value ratios have increased from around 55% to 66%, reflecting confidence in collateral liquidity. Even so, average LTVs remain conservative overall.

Management emphasised that this is not a structural shift in risk, as a material fall in gold prices would push LTVs back towards long-run averages rather than into stressed territory. Combined with modest average loan sizes and rapid loan turnover, this limits downside risk to both the balance sheet and earnings.

Jewellery retail

Jewellery retail includes both new and pre-owned items, with premium watches now a meaningful contributor. Pre-owned jewellery and watches typically carry higher margins and benefit from customer perceptions of tangible value, particularly during periods of economic uncertainty.

Growth in this area is constrained more by operations than demand. Refurbishment and repair, especially for watches, is skilled and time-consuming, limiting how quickly volumes can scale. Management is investing to improve throughput, but progress is incremental.

This division introduces some retail cyclicality, but it also supports higher margins.

Systems and technology

Ramsdens develops and maintains its core IT systems in-house, including its loan management platform, CRM and pricing tools. The group employs a small internal development team and does not rely on external software licensing for its core operating systems.

This approach supports incremental improvement rather than large, disruptive technology projects. Systems can be adapted quickly to changes in lending terms, pricing or regulatory requirements, and enhancements are rolled out across the estate without vendor dependency. While this does not create a technology moat, it improves operational control, reduces ongoing costs and supports consistency as the store estate expands.

Store economics and expansion

Store economics are an important part of understanding how scalable the model really is. Management disclosed that a new store typically requires around £500,000 of upfront investment. Of this, roughly £225,000 relates to establishing the store (fit-out, systems and setup), with the remaining £275,000 allocated to operations and initial inventory.

New stores are expected to reach profitability quickly, and some achieve this within their first year. This suggests the hurdle rate is not particularly high, but the group has been deliberately cautious on rollout. Fewer stores have been opened than originally planned, reflecting political uncertainty and operational constraints around staffing, training and management capacity.

There is no stated cap on the estate size, and management believes the store footprint could at least double over time. They point to examples of highly profitable stores in small catchment areas, including one in Scotland serving a population of around 10,000 that generated £180,000 in profit. The results presentation also identified more than 350 locations with populations above 30,000 as potential areas for further expansion. Even so, the focus remains on growing the estate conservatively and avoiding structural debt.

Store cost base and operating leverage

The cost base is largely fixed at the store level once a branch is established. Staffing, rent and security costs do not move in line with transaction volumes, which creates operating leverage when activity levels are high.

This has been evident over the past year, with higher volumes flowing through to profit more quickly than costs.

Balance sheet and capital discipline

The balance sheet remains a key strength. Despite increased lending balances and higher inventory levels, the group retains net cash and meaningful headroom. There is no reliance on long-term borrowing to support the pawnbroking book or inventory purchases.

This conservative capital structure underpins much of the operational flexibility discussed elsewhere: the ability to hold gold inventory, adjust loan-to-value ratios cautiously, and expand the store estate without taking balance sheet risk.

Net asset value has continued to grow, reflecting retained profits rather than financial leverage. This provides a tangible anchor for valuation and downside protection.

Management and execution

The overall impression from the results presentation and Investor Meet Q&A is of a management team that is cautious, pragmatic and operationally focused. Questions around gold price sensitivity, store rollout and forecasts were answered directly, without over-optimism or promotional language.

There is little evidence of a desire to chase growth for its own sake. Decisions around expansion, digital initiatives and product mix appear driven by returns and risk control rather than headline growth metrics. This does not guarantee superior outcomes, but it reduces the likelihood of strategic missteps.

Key risks and sensitivities

The most obvious sensitivity remains the gold price. Elevated prices have supported both volumes and margins, particularly in precious metals buying. A sharp reversal would reduce this contribution, though management’s emphasis on conservative lending and diversified income streams suggests the impact would be manageable rather than existential.

Regulatory risk exists, as with all consumer-facing financial services, but pawnbroking has historically faced less scrutiny than unsecured lending. Execution risk around store expansion and staffing is more relevant, but also more controllable.

Finally, after a strong share price run, valuation risk has increased. Even a well-run business can deliver disappointing returns if bought at the wrong price.

Sector consolidation

One of Ramsdens’ closest listed peers in UK pawnbroking, H&T Group, was taken private last year. The transaction provides a useful reference point for how established pawnbroking businesses with asset-backed lending, high cash conversion and limited credit risk have been valued in recent private market transactions.

The deal implied an enterprise value multiple of around 9.4 times operating profit, materially higher than where Ramsdens has typically traded. Management was clear in the Investor Meet Q&A that the acquisition has no bearing on Ramsdens’ strategy, but the transaction does highlight how the sector can be valued away from public markets.

The more relevant implication is that conservatively financed pawnbroking businesses can attract higher multiples in private ownership than those currently implied by public market pricing, particularly when earnings are cash-backed and balance sheets are strong.

Valuation assessment

After the re-rating, the shares no longer look obviously cheap. Much of the recent improvement in trading and profitability is now reflected in the rating, particularly given the supportive gold price backdrop.

That said, the valuation does not appear stretched when set against cash generation, balance sheet strength and the relatively low-risk nature of asset-backed lending. The question is less about whether the business is good, and more about how much further improvement is realistic from here.

Among brokers covering the stock, Cavendish Capital Markets recently raised its sum-of-parts target price from 480p to 490p. Spot gold prices are now meaningfully above the averages embedded in those models, suggesting the assumptions may be conservative. Ramsdens itself notes that the time from purchase to melt and sale typically takes around four weeks, a dynamic that can benefit realised margins in a rising gold market but works in reverse if prices fall.

Margin of safety

Viewed through a margin-of-safety lens, Ramsdens offers protection in several areas but less in others. The balance sheet is conservatively structured, earnings are asset-backed and diversified across four activities, and management has shown discipline in both expansion and capital use. These factors reduce the risk of permanent capital loss and provide resilience across different trading conditions.

A further, less obvious source of support is the hybrid nature of the model. Management noted that many customers now begin their journey online before completing transactions in store. The physical estate therefore reinforces digital activity by improving conversion, enabling immediate cash settlement and supporting inventory handling, rather than competing with it. This lowers execution risk and customer acquisition costs relative to purely online models. After the recent share price rise, however, the valuation buffer is limited, meaning the margin of safety rests more on business quality and operational resilience than on price alone.

Conclusion

Ramsdens comes out of FY25 looking like a stronger business than it was a year ago. The improvement is not confined to one line item: gross profit is now more evenly spread across precious metals, FX, pawnbroking and jewellery retail, and the operational choices described in the Q&A — cautious expansion, conservative funding and incremental system improvements — point to a management team focused on durability rather than short-term optimisation. The increase in pawnbroking loan-to-value ratios enhances returns at the margin, but remains within a conservative risk framework.

The central issue is sustainability. Recent profitability has clearly benefited from elevated gold prices, and a normalisation would reduce earnings. However, the business is not a simple gold proxy. Pawnbroking remains resilient under lower gold assumptions, FX provides steady income, and jewellery retail offers higher-margin optionality. The absence of structural debt, flexibility in inventory management and the hybrid online-to-store customer behaviour all strengthen earnings resilience and reduce execution risk.

Valuation is more balanced than compelling. After the re-rating, the shares no longer offer a wide discount to reasonable assumptions, so the margin of safety comes more from balance sheet strength, diversified earnings and conservative management than from price alone. Even so, current pricing does not appear aggressive when set against cash generation and private-market valuations for comparable pawnbroking assets.

Recommendation: Defensive buy.

Ramsdens offers a combination of steady cash generation, balance sheet protection and operational resilience that should appeal to investors seeking downside protection rather than rapid growth. Returns are likely to be incremental rather than spectacular, but the risk of permanent capital loss appears limited assuming continued disciplined execution.

The author owns shares in Ramsdens Holdings at the time of writing. This post is not advice.