Grainger: Strong Delivery as Property Sentiment Stabilises

At a time when UK property shares are still recovering from higher interest rates and policy uncertainty, Grainger’s latest trading update offers reassurance. Rents are rising steadily, homes remain largely full, and new developments continue to be delivered into a market where rental demand still exceeds supply. Against a backdrop of fragile sentiment toward real estate, that consistency matters.

The harder question is not whether Grainger plc is operating well, but how much of that quality is already recognised in the share price. The trading update confirms steady progress, but the valuation debate still hinges on how much confidence investors should place in reported asset values and future returns.

For the full margin-of-safety assessment and valuation framework:

Trading in line with expectations

Rental growth of 3.1 per cent year-to-date is in line with guidance, while occupancy of 96 per cent underlines continued demand across the portfolio. New schemes are letting quickly, including the Seraphina development in London, and additions to the pipeline support further growth. This is dependable execution rather than unexpected acceleration, but reliability remains an important asset in residential property.

Rental mix matters

Core PRS rental growth of 2.8 per cent is solid but not exceptional given recent inflation. The stronger 6.2 per cent growth in regulated tenancies lifts the blended figure, but this element of the portfolio is in run-off. The overall picture remains one of sustainable, mid-single-digit growth rather than a sharp improvement in pricing power.

Pipeline visibility

The key attraction remains earnings visibility. The committed development pipeline, now expanded through a joint venture scheme with Transport for London, provides a clear route to growth without relying on aggressive assumptions. Planned disposals of non-core assets are expected to release around £0.5bn of capital, helping fund development while keeping leverage under control.

Valuation and asset backing

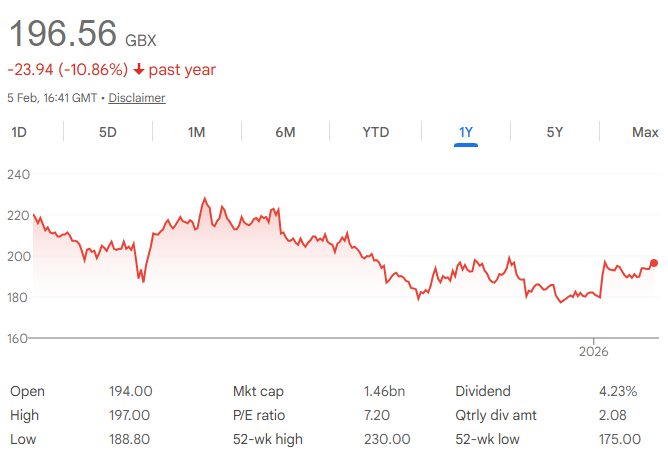

On the face of it, Grainger’s valuation looks supportive. Gross assets are around £3.8bn, set against roughly £1.7bn of debt, leaving just over £2bn of stated equity. With a market capitalisation of about £1.4bn, the shares trade at a material discount to reported net asset value.

That discount is the starting point for the valuation discussion, not its conclusion. Investors are implicitly questioning how durable those asset values are in a higher-rate world and what returns new development capital will ultimately generate. On reasonable assumptions, the combination of rental growth and pipeline delivery points to steady, mid-single-digit growth in cash flow, supplemented by a modest dividend. That supports the current valuation, but does not make the discount look anomalously wide given sector-wide scepticism toward property assets.

Margin of safety

Viewed through a Benjamin Graham lens, the margin of safety rests on asset backing, income resilience and balance sheet discipline.

On the positive side, Grainger owns residential property in supply-constrained UK cities, with high occupancy and diversified rental income. These characteristics support asset values and reduce earnings volatility. Planned disposals of non-core assets add financial flexibility, lowering the risk of forced sales or dilution.

The counterpoint is that the margin of safety is more operational than valuation-led. A plausible downside scenario would involve higher-for-longer interest rates, tighter regulation of rents, or slower lease-up of new developments. In such circumstances, asset values could soften and returns on new capital could fall. The balance sheet should be able to absorb that pressure, but the current share price discount may narrow only slowly, limiting near-term upside. The risk of permanent capital loss looks low, but the margin for error is not especially wide.

A Buffett-style view

From a Buffett perspective, Grainger looks like a good business available at a fair price rather than an obvious bargain. Expected shareholder returns are likely to come from a combination of modest income and steady compounding in asset values and earnings, rather than a sharp re-rating. That profile suits patient, long-term investors focused on capital preservation, but is less compelling for those seeking deep value or cyclical recovery upside.

Conclusion

On balance, Grainger continues to execute well in a structurally supportive market. Earnings growth is visible, the balance sheet is sound, and the asset base provides resilience. While the shares trade below stated net asset value, that discount reflects reasonable caution rather than clear mispricing.

Recommendation: Hold.

A move to Buy would likely require either a wider discount to net assets or clearer evidence that development returns and rental growth can sustainably exceed current assumptions. A shift to Sell would be driven by material policy intervention or a deterioration in funding conditions. Until then, the shares look fairly positioned for steady, unspectacular returns.

The author owns shares in Grainger at the time of writing. This post is not advice.